Understanding Student Finance in the UK

Thinking about higher education in the UK? Whether it’s university or college, figuring out how to pay for it is a big step. Thankfully, the UK government offers financial support to help students cover the costs. This system is known as Student Finance. It’s designed to make sure that finances don’t block people from gaining qualifications.

Let’s break down what you need to know about accessing and managing this support.

Who Can Get Student Finance? Checking Your Eligibility

The first question most people ask is: “Can I get this funding?” Understanding student finance eligibility is crucial. Generally, you need to meet certain criteria related to:

- Your Nationality and Residency Status: Usually, you need to be a UK national or have ‘settled status’, and you must normally live in the UK. Specific rules apply depending on where you live (England, Wales, Scotland, or Northern Ireland) and your circumstances. There are also provisions for EU nationals with settled or pre-settled status and some other specific groups.

- Your Course: The course you plan to study must be eligible. This includes most full-time undergraduate degrees (like a BA or BSc) and many postgraduate courses at approved universities or colleges. Part-time courses may also be eligible.

- Your Place of Study: The university or college must be registered and approved for student finance funding.

- Your Age: While there’s no upper age limit for Tuition Fee Loans, age can sometimes affect eligibility for Maintenance Loans or specific grants.

- Previous Study: If you’ve studied at a higher education level before, it might affect your eligibility for funding for a new course.

It’s always best to check the specific, detailed criteria on the official government website (gov.uk) for the part of the UK you live in, as rules can differ slightly.

What Funding is Available?

Student finance isn’t just one lump sum. It’s typically made up of different parts designed to cover specific costs:

Tuition Fee Loan:

- This loan covers the cost of your course fees, up to a certain limit depending on where you study in the UK.

- You don’t receive this money directly. It’s paid straight from the Student Loans Company (SLC) to your university or college.

- Most eligible UK students can get this loan, and it’s not based on your household income.

Maintenance Loan for Living Costs:

- This is the core support for day-to-day expenses while you study. Think rent, food, travel, books, and other living costs.

- The student finance maintenance loan is usually dependent on your household income (typically your parents’ income if you live with them or are financially dependent on them, or your own/partner’s income if you’re independent).

- Where you live while studying also makes a difference:

- Living at home usually means a lower loan amount.

- Living away from home (outside London) has a standard rate.

- Living away from home in London usually allows for the highest loan amount due to higher living costs.

- This money is paid directly into your bank account, usually in three instalments, one near the start of each term.

How Much Will I Get?

This is a very common question: “How much student finance will I get?” For the Tuition Fee Loan, it’s usually the full fee amount up to the cap. For the Maintenance Loan, it varies significantly based on the household income assessment and your living situation mentioned above.

To get an estimate, you can use the official student finance calculator available on the gov.uk website. This tool asks questions about your circumstances and gives you an indication of the loan amounts you might receive. It’s a great starting point for budgeting.

Extra Help:

- Depending on your circumstances, you might be eligible for additional grants or allowances that don’t usually need to be paid back. Examples include:

- Disabled Students’ Allowance (DSA) for help with costs related to a disability, long-term health condition, mental health condition, or specific learning difficulty.

- Grants for students with dependent children or adult dependents.

- Always check if you might qualify for this extra support.

The Application Process: Getting Started

Knowing how to apply for student finance is key. The process happens online through the official Student Finance website for your UK nation (England, Wales, NI, or Scotland).

When to Apply:

- Apply early! Applications usually open several months before courses start (often in the spring).

- There are deadlines. For example, the main student finance deadline 2025 (for courses starting in Autumn 2025) will likely be in late Spring 2025. Missing the deadline could mean your funding isn’t ready for the start of your course. Check the official dates for your year.

- You don’t need a confirmed university place to apply. You can use your preferred choice and update it later if needed.

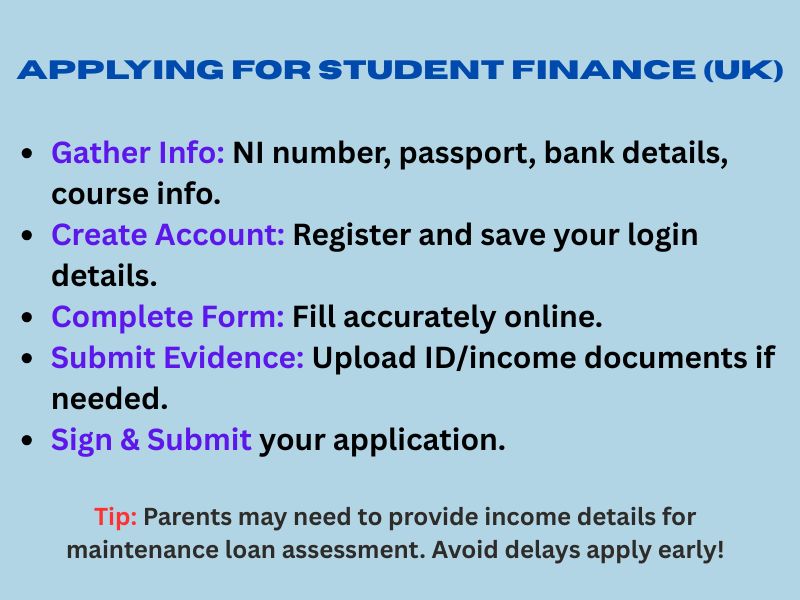

Steps to Apply:

- Gather Your Information: Before you start, have key details ready:

- Your National Insurance number.

- Your UK passport details (if you have one).

- Your bank account details.

- Your planned course and university details (even if provisional).

- If applying for the income-assessed Maintenance Loan, your parents or partner may need to provide their National Insurance numbers and details of their income (e.g., from P60s or tax returns).

- Create an Online Account: You’ll need to register on the Student Finance portal. This involves setting up a password and secret answer. Keep these safe!

- Complete the Application Form: Fill in all the required sections online. Be accurate and honest.

- Provide Supporting Evidence: You (and your parents/partner, if applicable) might need to submit evidence to support your application, such as proof of identity or income details. You can usually upload scanned copies directly through the online portal.

- Sign and Submit: Digitally sign and submit your completed application.

A Note for Parents:

If your child is applying for the income-assessed part of the maintenance loan, you’ll need to provide information about your household income. Student Finance will usually contact you directly or provide instructions via your child’s application. There’s helpful information available online, often framed as a student finance guide for parents, explaining your role in the process. Providing this information promptly helps avoid delays in your child’s funding assessment.

Verification and Account Setup:

- When setting up your online account, you’ll likely go through a verification step to securely link your online profile to your application records. This often requires your Customer Reference Number (CRN), which you’ll receive from Student Finance after applying, along with other identifiers like your date of birth.

- If you encounter issues verifying, double-check your details carefully. Sometimes you just need to wait a little longer for the system to fully update after you first apply.

Managing Your Student Finance Online

Once your application is approved and you have your online account set up, this portal becomes your main hub for managing your student finance.

- Your Customer Reference Number (CRN): This unique number identifies you. Keep it safe and use it when contacting Student Finance.

- What You Can Do: Log in using your CRN, password, and secret answer to:

- Check the status of your application.

- View your payment schedule (once confirmed).

- Update your details (like address or bank account). Crucially, keep your bank details correct to ensure you receive payments.

- View correspondence and letters from Student Finance.

- Upload any requested evidence.

- Common Login Issues: If you forget your CRN, password, or secret answer, use the recovery links on the login page. If your account gets blocked, you may need to contact Student Finance directly.

Specific Situations: Master’s Degrees and Benefits

Student Finance for Master’s:

- Thinking of postgraduate study? There is separate student finance for master’s degrees available in the UK.

- This usually takes the form of a single loan payment that can contribute towards both fees and living costs.

- The eligibility criteria and loan amounts differ from undergraduate finance. For instance, the loan amount is generally not based on household income but has a maximum cap. Repayment rules are also slightly different. Check the specific postgraduate loan details for your UK nation.

Student Finance and Universal Credit:

- If you receive Universal Credit (UC), you need to understand the interaction between student finance and Universal Credit.

- Generally, some parts of the Maintenance Loan (but not the Tuition Fee Loan or specific grants like DSA) may be counted as income when calculating your Universal Credit award.

- It’s vital to report your student finance details accurately and promptly to the Department for Work and Pensions (DWP) to ensure your UC payments are correct. Always seek official advice from gov.uk or DWP if you’re unsure how your student finance affects your benefits.

Paying Back Your Student Loan: Understanding Repayment

The thought of repaying loans can be daunting, but the UK system is designed to be manageable. Here’s how student finance repayment works:

- You Only Repay When You Earn Enough: You won’t start repaying until your income is over a certain threshold. This threshold depends on which ‘Repayment Plan’ you are on (which itself depends on when and where you studied and what type of loan you took out).

- Repayments are Income-Contingent: You repay 9% of your income above the threshold, not 9% of your total salary. If your income drops below the threshold, your repayments stop automatically.

- Automatic Deductions: If you’re employed, repayments are usually taken automatically from your salary through the tax system (Pay As You Earn – PAYE), just like income tax and National Insurance. If you’re self-employed, repayments are handled through your Self Assessment tax return.

- Interest: Interest is charged on your loan from the time you receive your first payment. The rate varies depending on your Repayment Plan and current circumstances (e.g., while studying vs. after graduating, and your income level).

- Loan Write-Off: Student loans are eventually written off after a set period (e.g., 25, 30, or 40 years after you become eligible to repay), even if you haven’t paid them all back. The exact period depends on your Repayment Plan.

- Not Like Commercial Debt: Importantly, student loan debt doesn’t typically affect your credit score in the same way as commercial loans like credit cards or mortgages. However, mortgage lenders might ask about your student loan repayments when assessing affordability.

Key Takeaways

Navigating student finance can seem complex initially, but it’s a supportive system designed to help you invest in your future. Remember:

- Check your eligibility carefully.

- Apply early and meet the deadlines.

- Use the online tools like the calculator and portal effectively.

- Keep your details updated.

- Understand how repayment works – it’s linked to your earnings.

Always refer to the official gov.uk website for the most accurate and up-to-date information specific to your circumstances and the part of the UK you live in. With careful planning, student finance can be a manageable part of your higher education journey.

Read more about UK Education Loans for International Students – Complete Guide

Frequently Asked Questions

Yes, household income usually affects the amount of Maintenance Loan (for living costs) you get, but not the Tuition Fee Loan.

Apply early, well before the official student finance deadline (e.g., Spring for Autumn start). You don’t need a confirmed offer to apply – you can update your course details later.

You only start student finance repayment after finishing your course and earning above the set income threshold for your loan plan.

No, UK student loans don’t directly impact your credit score like other debts. However, lenders might consider repayments when assessing mortgage affordability.

Use the ‘forgotten details’ links on the official login page to recover your CRN, password, or secret answer. Contact Student Finance if you still have trouble.

Source / Ref.: Gov.uk Gov.uk Contains public sector information licensed under Open Government Licence v3.0.

Written by [Ketan Borada / British Portal Team] – Founder of British Portal, dedicated to providing accurate and up-to-date information on UK public services and benefits.Related Posts

Previous Post

Next Post

- Business

5

5 - Cricket5

- Department for Education49

- Departments3

- Driving and Transport

53

53 - Education45

- Finance6

- Football13

- Golf3

- Government

108

108 - Guides1

- Health4

- Health

5

5 - International Politics9

- Law and Justice31

- Money and Tax23

- National Politics4

- News68

- Politics6

- Sports38

- Technology5

- Tennis3

- Transportation4

- Uncategorized4

- Visa

17

17 - Visas and Immigration

24

24 - Weather1