Understanding how trusts work can save you thousands in taxes while protecting your family’s future. Trusts aren’t just for the wealthy – they’re practical tools that many UK families use to manage their assets wisely.

What Are Trusts and Why Should You Care?

Trusts might sound complicated, but they’re quite simple. A trust is just a legal way to hold and manage assets for people. Think of it as a protective container for your money, property, or investments.

Three key people are involved in any trust. The ‘settlor’ is the person who puts assets into the trust. The ‘trustee’ manages everything and makes decisions. The ‘beneficiary’ is the person who benefits from the trust – income, property, or money.

Why create a trust? People set them up for many reasons. You might want to protect family assets from being spent unwisely. Maybe you have children too young to handle money. Perhaps you need to provide for someone who can’t manage their affairs due to illness. Trusts also offer ways to pass on assets while you’re alive or after you die.

How a Property Trustee Works

Being a trustee for property means you’re legally responsible for managing buildings or land according to the trust’s rules. As a property trustee, you must make decisions that benefit the people named in the trust. This might include collecting rent, arranging repairs, or deciding when to sell.

Many families appoint trusted family members as trustees, but you can also use professionals like solicitors or accountants if the situation is complex.

Trusts and Inheritance Tax: The Big Money Saver

Inheritance tax hits many UK families hard. Currently charged at 40% above certain thresholds, it can take a significant chunk of your estate. This is where understanding trust inheritance tax rules becomes valuable.

Some people use trusts to avoid inheritance tax legally. These trust funds to avoid inheritance tax must be set up correctly and well in advance. The timing matters – if you die within seven years of putting assets into some types of trusts, inheritance tax might still apply.

Inheritance from Trust: Is It Taxable?

When beneficiaries receive money or assets from a trust, they often ask about the inheritance from the trust’s taxable status. The answer depends on the type of trust and how it was set up.

With some trusts, beneficiaries pay income tax on any income they receive. With others, the trust itself pays the tax. Trust fund inheritance tax can be lower than personal inheritance tax in some cases, which makes trusts attractive for estate planning.

If you’re dealing with larger estates, you might hear about GSTT (Generation-Skipping Transfer Tax) considerations, especially when planning to transfer wealth across multiple generations.

As you plan for inheritance tax, it’s equally important to stay updated on upcoming changes in UK Inheritance Tax Planning for 2025 to ensure your financial strategies align.

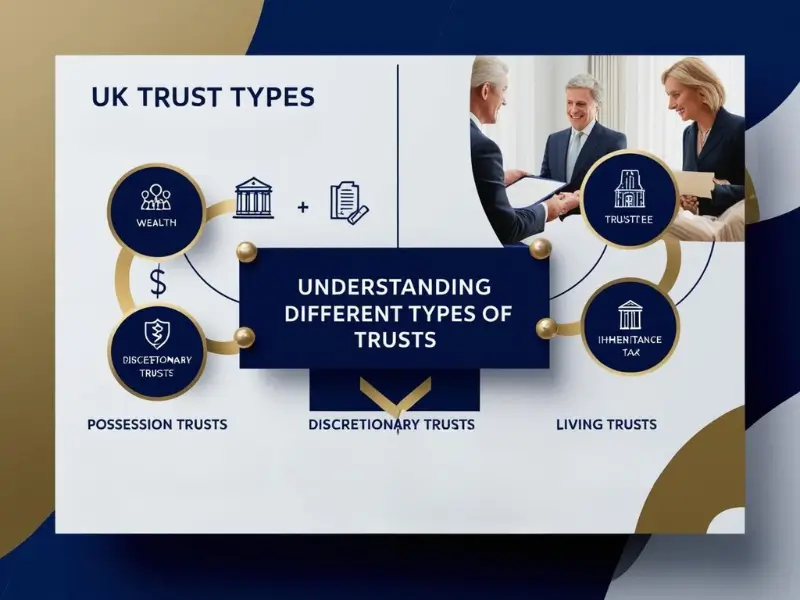

Different Types of Trusts for Different Needs

Not all trusts work the same way. The type you choose affects both control and the taxation of trusts.

Interest in Possession Trusts

Interest in possession trusts gives someone the right to benefit from the trust right away. For example, your spouse might receive income from your investments while you specify that the capital goes to your children later. These trusts have specific inheritance tax rules and can be useful for providing for different generations.

Discretionary Trust Inheritance Tax Considerations

A discretionary trust inheritance tax treatment differs from other types. These trusts give trustees complete power to decide who gets what and when. This flexibility comes at a price – they often face higher tax rates. However, they’re excellent when you want maximum control over how your assets are distributed, perhaps for children or grandchildren with varying needs.

Living Trust Inheritance Tax Benefits

A living trust is created while you’re still alive. Living trust inheritance tax planning can help reduce your estate’s tax burden while ensuring your wishes are carried out exactly as you want. These can be especially useful if you own properties in different countries or have complex family situations.

Capital Gains Tax and Trusts: Another Key Consideration

It’s not just inheritance tax you need to think about. Trusts and capital gains tax have a special relationship.

When assets in a trust increase in value and are sold, capital gain in trust situations can trigger tax bills. The rules for trust fund capital gains tax often differ from personal CGT rates.

CGT for trusts currently stands at higher rates than for individuals in many cases. CGT and trusts an area where planning pays off. For example, timing the sale of assets can make a significant difference to the tax bill.

Trust Taxes: The Overall Picture

The taxability of trusts varies depending on the type and how they are managed. Some trusts pay tax directly on the income they receive. Others pass the tax liability to beneficiaries.

The taxation of trusts can seem complex, but with good advice, you can navigate it successfully. The tax treatment of trusts includes various reliefs and exemptions worth exploring with a professional.

Important Forms and Reporting Requirements

If you’re managing a trust, you’ll need to deal with paperwork. The IHT100 form is used for reporting certain trust charges to HMRC. Another form, IHT418, relates to assets leaving a trust. Don’t let these forms intimidate you – they’re just part of the process.

Trusts have their own tax returns and reporting requirements. Missing deadlines can result in penalties, so keeping good records is essential.

Real-Life Trust Scenarios

Let’s look at how trusts work in everyday situations:

Sarah and John want to ensure their holiday home passes to their children without a massive inheritance tax bill. By placing it in a trust, they might reduce future tax bills while ensuring the property stays in the family.

Michael has a child with support needs. A trust ensures his daughter will be cared for financially even after he’s gone, with trustees making decisions in her best interest.

Elizabeth wants her grandchildren to benefit from her investments but only when they’re mature enough. A discretionary trust gives her trustees the power to decide when the time is right.

Is a Trust Right for You?

Trusts and tax planning go hand in hand, but trusts aren’t just about saving tax. They’re about control, protection, and ensuring your wishes are respected.

If any of these situations apply to you, a trust might be worth considering:

- Do you have children or grandchildren you want to provide for

- You own a business you want to keep in the family

- You’re worried about care home fees eating up your assets

- You want to control how and when beneficiaries receive your assets

- You have a complex family situation such as second marriages

Getting Started with Trust Planning

If you’re thinking about setting up a trust, start by being clear about what you want to achieve. Is it protecting assets? Saving tax? Providing for vulnerable family members?

Once you know your goals, professional advice is essential. Tax rules change frequently, and what worked for your friend might not work for you.

Remember that while trusts can help with tax planning, they’re primarily about control and protection. Don’t focus only on tax savings – think about the bigger picture of what you want for your family’s future.

Takeaway

Trusts offer a powerful way to protect your assets and care for loved ones while potentially reducing tax bills. Whether you’re concerned about trust inheritance tax, capital gains tax for a trust, or simply want more control over your assets, trusts provide solutions worth exploring.

With the right planning, you can create arrangements that work for your family while keeping tax bills as low as legally possible. The peace of mind that comes from knowing your wishes will be carried out as you intend is perhaps the greatest benefit of all.

FAQs

1. What are the tax implications of trusts?

Trusts can incur various taxes, including income tax, capital gains tax (CGT), and inheritance tax (IHT). The specific tax treatment depends on the type of trust and how it is structured. For instance, discretionary trusts are subject to different rates than interest in possession trusts.

2. How does inheritance tax apply to trusts?

Inheritance tax is generally due when assets are transferred into a trust if their value exceeds the nil rate band of £325,000. Additionally, IHT may be charged every ten years on the value of the trust’s assets.

3. Are distributions from a trust taxable?

Yes, distributions from a trust can be taxable. Beneficiaries may owe income tax on amounts received from the trust, depending on the type of trust and how income is distributed.

4. What is the annual exemption for capital gains tax on trusts?

Trusts have a lower annual exemption for capital gains tax compared to individuals. As of the 2023/24 tax year, the annual exempt amount for trusts is £6,000.

5. Do trustees need to file tax returns?

Yes, trustees must file a Self-Assessment tax return for the trust, even if no tax is due. This includes reporting income and gains and providing details about distributions to beneficiaries.

Source / Ref.: Gov.uk Contains public sector information licensed under Open Government Licence v3.0.

Written by [Ketan Borada / British Portal Team] – Founder of British Portal, dedicated to providing accurate and up-to-date information on UK public services and benefits.Related Posts

Previous Post

Next Post

Previous Post

Next Post

- Business

5

5 - Cricket5

- Department for Education49

- Departments3

- Driving and Transport

53

53 - Education45

- Finance6

- Football13

- Golf3

- Government

108

108 - Guides1

- Health

5

5 - Health4

- International Politics9

- Law and Justice31

- Money and Tax23

- National Politics4

- News68

- Politics6

- Sports38

- Technology5

- Tennis3

- Transportation4

- Uncategorized4

- Visa

17

17 - Visas and Immigration

24

24 - Weather1