The UK tax system funds our essential public services, but not all taxes owed are collected. This difference is what experts call the “tax gap” – the shortfall between taxes that should be paid and what reaches government coffers. Recent HMRC figures reveal fascinating insights into this financial phenomenon affecting every UK citizen.

What is the Tax Gap and Why Should You Care?

The tax gap is the difference between the taxes that should be paid and what is collected. This gap can occur for many reasons, including honest mistakes and intentional tax evasion.

While the term may sound boring, it has real consequences. The tax gap affects funding for important services like schools and hospitals. When some people don’t pay their fair share of taxes, others have to pay more, or public services get less money.

That’s why it’s important to understand the tax gap in the UK. It matters to everyone, whether you are self-employed, running a business, or an employee paying taxes through PAYE (Pay As You Earn).

The UK Tax Gap in 2023

The latest figures indicate that the UK tax gap—the difference between the theoretical tax liability and the amount collected by HMRC—was estimated at £39.8 billion for the 2023-2024 tax year, representing a slight increase compared to previous years. This figure reflects ongoing challenges in reducing tax losses, despite government efforts to address evasion and avoidance.

In response to this rising gap, HMRC announced a £1.6 billion investment over five years to recruit 5,000 additional compliance officers and 1,800 debt management officers, with initial recruitments beginning in late 2024. This initiative aims to enhance enforcement and compliance measures across various sectors.

Additionally, revisions to VAT receipts for the 2022-2023 tax year have led to adjustments in the VAT gap estimates, which will be included in HMRC’s upcoming “Measuring Tax Gaps” publication in June 2025. These revisions are expected to impact overall tax gap calculations for previous years.

While the long-term trend since 2005 has shown a reduction in the percentage of the tax gap relative to theoretical liabilities, recent economic uncertainties and methodological updates continue to influence these figures. Further updates are anticipated later this year as HMRC refines its estimates and strategies

Breaking Down the HMRC Tax Gap

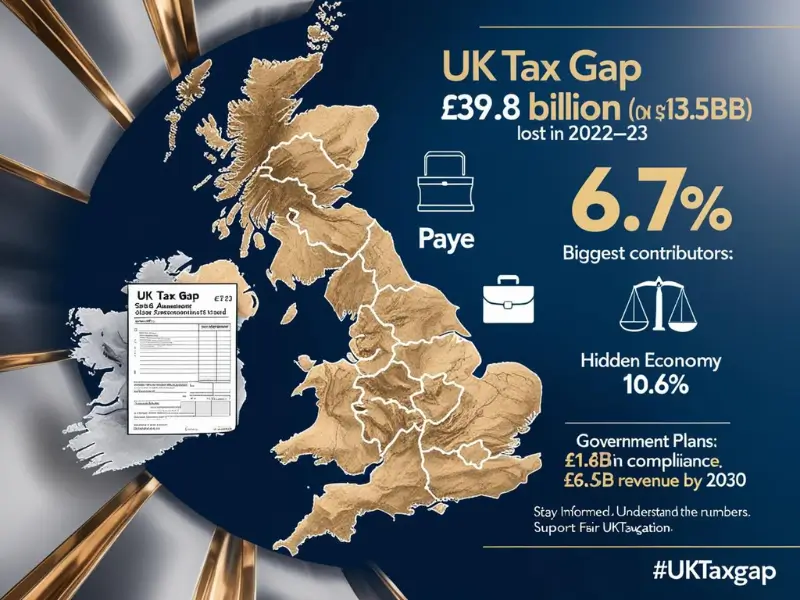

The analysis of the HMRC tax gap reveals significant insights into the components contributing to uncollected taxes. As of the most recent estimates, the overall tax gap stands at approximately £39.8 billion for the 2022-2023 tax year, which represents 4.8% of the total theoretical tax liabilities.

Components of the Tax Gap:

- Self-Assessment: This category constitutes the largest portion of the tax gap at 61.7%. The biggest contributor, with £8.5 billion in unpaid taxes from self-employed individuals and small businesses. Although this figure has decreased from 15.1% in 2005-2006, it still indicates a substantial loss to public finances.

- PAYE Employer Compliance: This accounts for 23.9% of the total tax gap. Businesses failing to report payroll taxes contribute £9.5 billion to the tax gap.

- Hidden Economy: Individuals working completely off the books contribute 10.6% to the tax gap, emphasizing ongoing issues with unreported income.

- Tax Avoidance Schemes: These schemes represent 3.8% of the total gap, reflecting efforts to exploit legal loopholes to minimize tax liabilities.

In response to these challenges, HMRC has initiated a significant investment strategy. HMRC plans to close the tax gap with a £1.6 billion investment over five years to hire more compliance staff.This effort aims to improve HMRC’s ability to tackle non-compliance, particularly among small businesses, which accounted for 60% of the tax gap in 2022-2023.

Looking forward, HMRC’s strategic objectives include enhancing compliance activities and leveraging digital services to streamline tax collection processes. HMRC’s new compliance measures are expected to recover £6.5 billion per year by 2029-2030.

Small Business and VAT: Where the Gaps Widen

The small business tax gap has grown, with self-employed taxpayers. Small partnerships contribute to a 24.3% gap in their tax liability, totaling about £5.9 billion for the 2022-2023 tax year. This alarming figure suggests that nearly a quarter of taxes owed by small businesses are not being collected by HMRC.

Recent data indicates that small businesses account for 60% of the tax gap, up from 44% five years ago. This highlights the increasing compliance challenges HMRC faces with smaller enterprises, particularly regarding complex VAT regulations. While specific VAT gap figures weren’t provided, it remains a significant area for both unintentional non-compliance and deliberate evasion.

The percentage of self-assessment returns with under-declared tax rose from about 23% (2016-2020) to 30% in 2021. Most under-declarations involve relatively small amounts, typically under £5,000.

In response to these challenges, HMRC is implementing a robust strategy to address non-compliance among small businesses. The government has allocated funding for 5,000 compliance officers and 1,800 debt management staff to enhance tax enforcement and collection. These efforts aim to generate an extra £6.5 billion in tax revenue annually by 2029-2030.

Moreover, the Corporation Tax gap for small businesses has reached an estimated 32.2% of their theoretical Corporation Tax liability, translating to around £10.9 billion in absolute terms for the 2022-2023 tax year. This reflects a significant increase from previous years and highlights the need for improved compliance measures.

HMRC’s efforts to reduce the tax gap for small businesses aim to improve compliance and secure funding for public services.

The Hidden Economy: Working in the Shadows

The hidden economy in the UK significantly contributes to the overall tax gap, which is currently estimated at £39.8 billion for the 2022-2023 tax year, representing 4.8% of total theoretical tax liabilities. This gap includes two primary groups: “moonlighters,” who earn additional income without declaring it, and “ghosts,” who operate entirely off HMRC’s radar. Together, these groups account for approximately 10.6% of the total tax gap.

Key Insights:

- Moonlighters and Ghosts: HMRC rates the uncertainty in estimating the contributions of moonlighters as “high” and ghosts as “very high,” due to their deliberate efforts to remain hidden from tax authorities.

- Impact on Revenue: The hidden economy is a significant challenge for HMRC, with estimates suggesting that nearly 9% of UK adults participate in this shadow economy. This participation leads to substantial losses in tax revenue, as evasion-type behaviors are responsible for about 30% of the total tax gap.

- Excise Tax Gaps: Similar issues are observed in excise taxes related to products like alcohol, tobacco, and fuel, where smuggling and counterfeit goods contribute to lost revenue; however, specific figures on these gaps are not detailed in recent data.

Government Response:

In response to the challenges posed by the hidden economy, HMRC has announced a £1.4 billion investment aimed at enhancing compliance efforts. This includes recruiting additional compliance staff and modernizing systems to improve the detection of non-compliance and evasion. The government aims to raise an additional £6.5 billion in tax revenue annually by 2029-2030 through these initiatives.

Closing the Tax Gap: The Road Ahead

Efforts to close the tax gap in the UK are evolving, with a focus on enhancing compliance and utilizing technology to address deliberate evasion. Here are the latest updates on this critical issue:

Current Tax Gap Overview

- The estimated tax gap for 2022-2023 is £39.8 billion, which equals 4.8% of total tax liabilities. This marks a significant recovery, as HMRC collected 95.2% of all taxes due during this period.

Compliance Recovery Efforts

- HMRC’s compliance activities successfully recovered approximately £1.5 billion from self-assessment taxpayers in the 2022-2023 tax year, contributing to a reduction in the net tax gap.

Gender Tax Gap

- While not directly reflected in the overall tax gap statistics, the gender tax gap is gaining attention in discussions about tax fairness and equity. It emphasizes the need to tackle ongoing disparities in broader tax reform efforts.

Role of Technology

- Technology is playing an increasingly vital role in improving tax collection efficiency. HMRC is leveraging digital reporting requirements and advanced data analytics to identify potential non-compliance earlier and more accurately. The agency’s system, known as ‘Connect,’ analyzes over 50 billion lines of data, enabling better targeting of compliance efforts.

Government Initiatives

- The UK government announced new resources to address the tax gap. The Autumn Statement 2023 introduced a package designed to raise £5 billion over five years through enhanced compliance measures and support for taxpayers facing debt.

- The Labour Party pledged £855 million annually to HMRC to improve tax collection and IT systems.

Future Projections

- HMRC aims to raise £6.5 billion in five years by hiring 5,000 compliance officers and improving digital taxpayer services.

These developments reflect a comprehensive approach to closing the tax gap while addressing various dimensions of tax compliance and equity.

What This Means for You

Whether you’re an employee, self-employed, or a business owner, the tax gap affects you. When taxes go uncollected, it creates pressure to either raise rates or reduce services. Fair taxation depends on everyone paying their share.

Understanding the components of the tax gap helps us recognize where the system needs improvement. Whether through simpler rules for small businesses, better education about tax obligations, or stronger enforcement against deliberate evasion.

The next time you hear discussions about public spending or tax rates, remember the tax gap statistics.

By understanding these figures, we can better engage in the national discussion on funding shared priorities and ensuring fair contributions.

Read more about Tax Overpayments and Underpayments: Tips to Save Money Now!

FAQs

1. What is the tax gap in the UK?

The tax gap in the UK is the difference between the amount of tax that should be collected by HM Revenue and Customs (HMRC) and what is actually collected. For the 2022-2023 tax year, this gap is estimated to be £39.8 billion, which represents about 4.8% of the total theoretical tax liability.

2. What are the main causes of the tax gap?

The tax gap arises from several factors, including criminal behavior (like tax evasion), errors made by taxpayers, non-payment of taxes, and differences in legal interpretation regarding tax obligations. Approximately 58% of the gap is attributed to criminal behavior and lack of reasonable care.

3. How does the UK tax gap compare to other countries?

Comparing the tax gap by country can be challenging due to different tax systems and measurement methods. However, many countries face similar issues with tax compliance. For instance, the US also experiences a significant tax gap, highlighting a common challenge in ensuring all taxpayers meet their obligations.

4. What steps are being taken to close the tax gap?

The UK government and HMRC are implementing strategies to close the tax gap, such as improving compliance measures, simplifying tax regulations for small businesses, and enhancing data analysis capabilities to identify non-compliance earlier.

5. How accurate are tax gap estimates?

HMRC calculates the tax gap based on available data and methodologies approved by the UK Statistics Authority. While these estimates are generally reliable, they come with uncertainty ratings, indicating that some components of the tax gap may have high levels of uncertainty due to limitations in data collection and analysis methods.

Source / Ref.: Gov.uk Gov.uk Contains public sector information licensed under Open Government Licence v3.0.

Written by [Ketan Borada / British Portal Team] – Founder of British Portal, dedicated to providing accurate and up-to-date information on UK public services and benefits.Related Posts

Previous Post

Next Post

- Business

5

5 - Cricket5

- Department for Education49

- Departments3

- Driving and Transport

53

53 - Education45

- Finance6

- Football13

- Golf3

- Government

108

108 - Guides1

- Health4

- Health

5

5 - International Politics9

- Law and Justice31

- Money and Tax23

- National Politics4

- News68

- Politics6

- Sports38

- Technology5

- Tennis3

- Transportation4

- Uncategorized4

- Visa

17

17 - Visas and Immigration

24

24 - Weather1