Public Authorities Bill: Key Changes Targeting UK Fraud & Error

Big changes are potentially on the way for how the UK government tackles fraud and mistakes in the benefits system. Major plans to save taxpayers £1.5 billion have taken a significant step forward. Ministers are pushing for new powers to recover stolen cash and clamp down on those who wrongly receive public money. The Public Authorities (Fraud, Error and Recovery) Bill has just passed a key stage in the House of Commons and now moves to the House of Lords for further checks. This development is part of what the government calls its “Plan for Change,” aiming to ensure taxpayer funds are used correctly and can be better invested in public services we all rely on.

Why is This Happening Now? The Push for Change

The government states these new measures are needed to fix what they describe as “unacceptable levels of fraud and error.” Official figures suggest these issues cost the UK taxpayer around £10 billion every single year. Since the pandemic began, it’s estimated that a staggering £35 billion has been paid out incorrectly from the Department for Work and Pensions (DWP) alone. The UK Fraud Bill aims to modernise tools to detect and prevent losses.

Minister for Transformation, Andrew Western, highlighted the need, saying,

“Enhancing our powers is essential… to address the unacceptable levels of fraud and error we’ve inherited and better protect public funds.”

The goal is clear: update the system to catch dishonest claims and correct mistakes faster.

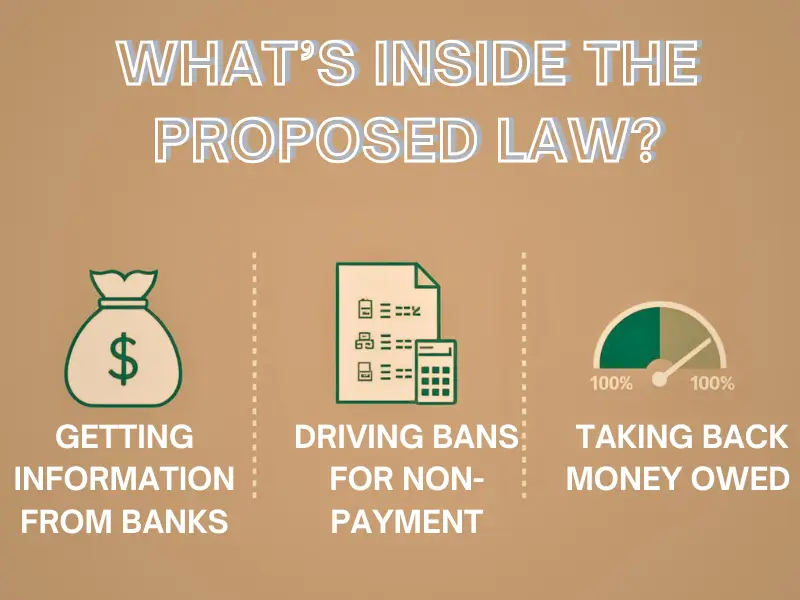

What’s Inside the Proposed Law? A Closer Look at the Powers

This bill includes several new tools and powers, mainly for the DWP, the department handling benefits like Universal Credit. Let’s break down the main parts:

Getting Information from Banks (Data Sharing)

- The bill gives the DWP the power to ask banks and other financial institutions for certain information.

- Purpose: This is to help check if someone claiming benefits is eligible. For example, it could help spot if someone has savings above the allowed limit for certain benefits.

- Privacy Concerns Addressed: This has raised some questions about privacy. However, the government insists DWP will not get access to people’s bank accounts or see how they spend their money day-to-day. They will only receive limited data signals specifically related to eligibility rules. No personal information will be shared by DWP with the banks for this purpose. The goal is to catch fraud or errors early and prevent claimants from being overpaid and falling into debt.

Taking Back Money Owed (Direct Recovery)

- A significant new power would allow the DWP to recover money directly from the bank accounts of people who owe debt due to fraud or error.

- Who does this affect? This power is specifically targeted at individuals who can afford to repay the money but are deliberately avoiding it – what the government calls “wilfully gaming the system.”

- Safeguards: This isn’t intended as a first step. It’s presented as a tool to be used when other attempts to recover the debt have failed, focusing on those deliberately refusing to pay back money they weren’t entitled to. This is a key part of the plan to recover the stolen cash bill UK.

Driving Bans for Non-Payment (A Last Resort)

- Perhaps the most talked-about measure is the power to disqualify people from driving if they persistently fail to repay fraud-related debts.

- Strict Conditions: Officials stress this Driving Ban Fraud Bill measure would only be used as a last resort.

- Exemptions: Crucially, it would not apply if the person relies on their car for their job or essential caring responsibilities.

- Fairness: The idea is to use this as leverage against those who can pay but won’t, ensuring fairness to the taxpayer. Staff will receive specific training, and there will be oversight to ensure this power is used appropriately.

Tackling Covid-Related Fraud Head-On

The pandemic saw a huge increase in government spending and, unfortunately, opportunities for fraud. This bill specifically addresses that:

- More Time to Investigate: Authorities now have 12 years, instead of six, to take civil action against Covid fraudsters.

- Why? Complex fraud cases take time to unravel. This extension gives investigators, including the Covid Corruption Commissioner and the Public Sector Fraud Authority, more time to use these new powers (like recovering money from bank accounts) even for fraud committed during the pandemic years.

Strengthening the Watchdogs: The Public Sector Fraud Authority (PSFA)

It’s not just the DWP getting new tools. The bill also boosts the powers of the Cabinet Office’s Public Sector Fraud Authority (PSFA).

- Wider Reach: PSFA investigators will gain more authority to detect and recover fraud not just within the DWP, but across other government departments and public bodies too.

Minister Georgia Gould stated,

“This Bill will save taxpayers’ money… We’re giving our investigators new powers to tackle fraud wherever they find it.”

More Staff, More Checks

Alongside the new legal powers, the government is also investing in people. Over 500 additional DWP staff focused on fraud and error are being recruited. They will use improved data analysis techniques to correct mistakes in benefit claims and increase checks on things like savings and earnings for Universal Credit applicants.

What are the Big Goals? £1.5 Billion Savings and Fairer Systems

The headline figure is the £1.5 billion the government expects this Fraud Bill UK to save over the next five years. This is part of a much larger government target to save £9.6 billion through various anti-fraud and error measures by 2030. The message is that clamping down on losses means more money available for vital public services.

The goal is to make the system fairer, protecting taxpayers’ money and reducing errors that hurt genuine claimants. The focus is clearly on distinguishing between genuine mistakes and deliberate benefit fraud bill UK attempts.

What Happens Next?

The bill, sometimes referred to broadly as the Fraud Error and Debt Bill in the UK, has successfully passed its stages in the House of Commons. This included the important “Third Reading.“

Now, the Fraud Bill House of Lords stage begins. Members of the House of Lords will carefully examine the bill, debate its contents, and potentially suggest changes (amendments). This scrutiny is a standard part of the UK law-making process. Only after it passes through the Lords (potentially returning to the Commons if changes are made) and receives Royal Assent can it become official law. The Fraud Bill 2024 of the UK is therefore still under review.

A Significant Shift in Tackling Fraud

The UK’s Public Authorities (Fraud, Error, and Recovery) Bill aims to tighten control over fraud and error in welfare and the public sector. New powers like data sharing, debt recovery, and driving bans aim to strengthen public fund management and fight COVID fraud.

The government backs these tools to fight fraud, but debates on privacy and impacts on vulnerable people will continue in the Lords. The coming weeks and months will be crucial in shaping the final details of this significant piece of legislation. Its eventual impact on saving public money and ensuring the benefits system operates fairly will be closely watched.

Read more about How to Report Benefit Fraud in the UK

Frequently Asked Questions

The plan isn’t for DWP to browse accounts. Banks will only share limited, automated signals indicating if an account holder might breach eligibility rules (like having too much savings). DWP won’t see transaction lists or balances, just flags requiring further checks.

No. This ‘direct recovery’ power is described as a last resort, targeted at those deliberately avoiding repayment of proven fraud/error debt who can afford to pay. Other recovery methods would typically be attempted first.

Specific details are pending, but the DWP would assess individual circumstances. Exemptions are stated for those relying on a vehicle for work or significant caring responsibilities. Evidence would likely be required.

While DWP powers focus on benefit claimants, the bill also expands the Public Sector Fraud Authority’s (PSFA) powers. This means PSFA investigators can tackle fraud in other government departments and public bodies, broadening the scope beyond just welfare.

The bill must first pass the House of Lords and receive Royal Assent to become law. After that, implementation (including staff training and system setup) will take time. It won’t be immediate, likely happening gradually once the law is fully enacted.

Source / Ref.: Gov.uk Contains public sector information licensed under Open Government Licence v3.0.

Written by [Ketan Borada / British Portal Team] – Founder of British Portal, dedicated to providing accurate and up-to-date information on UK public services and benefits.Related Posts

Previous Post

Next Post

- Business

5

5 - Cricket5

- Department for Education49

- Departments3

- Driving and Transport

53

53 - Education45

- Finance6

- Football13

- Golf3

- Government

108

108 - Guides1

- Health4

- Health

5

5 - International Politics9

- Law and Justice31

- Money and Tax23

- National Politics4

- News68

- Politics6

- Sports38

- Technology5

- Tennis3

- Transportation4

- Uncategorized4

- Visa

17

17 - Visas and Immigration

24

24 - Weather1