HGV levy is a mandatory tax for heavy goods vehicles (HGVs) driving on UK roads. It’s often confused with HGV road tax, but both serve different purposes. Understanding the difference is crucial for operators, transport businesses, and drivers managing registered vehicles.

In the UK, HGVs are subject to both tax levies and Vehicle Excise Duty (VED). These charges help maintain infrastructure and ensure fairness between domestic and international hauliers. With UK vehicles over 12 tonnes required to pay the levy, knowing how it’s calculated, paid, and checked is vital.

Let’s explore what the HGV levy covers, how it’s different from HGV road tax, and what changes are expected by 2025.

The HGV Levy

Purpose

The HGV levy was introduced in 2014 to ensure that heavy goods vehicles (HGVs) contribute fairly to the maintenance and development of the UK’s road infrastructure.

It applies to vehicles with a gross weight of 12,000 kg or more, encompassing both UK-registered and foreign-registered vehicles operating on UK roads.

The primary objective is to level the playing field between domestic and international hauliers, ensuring that all pay their share for road usage.

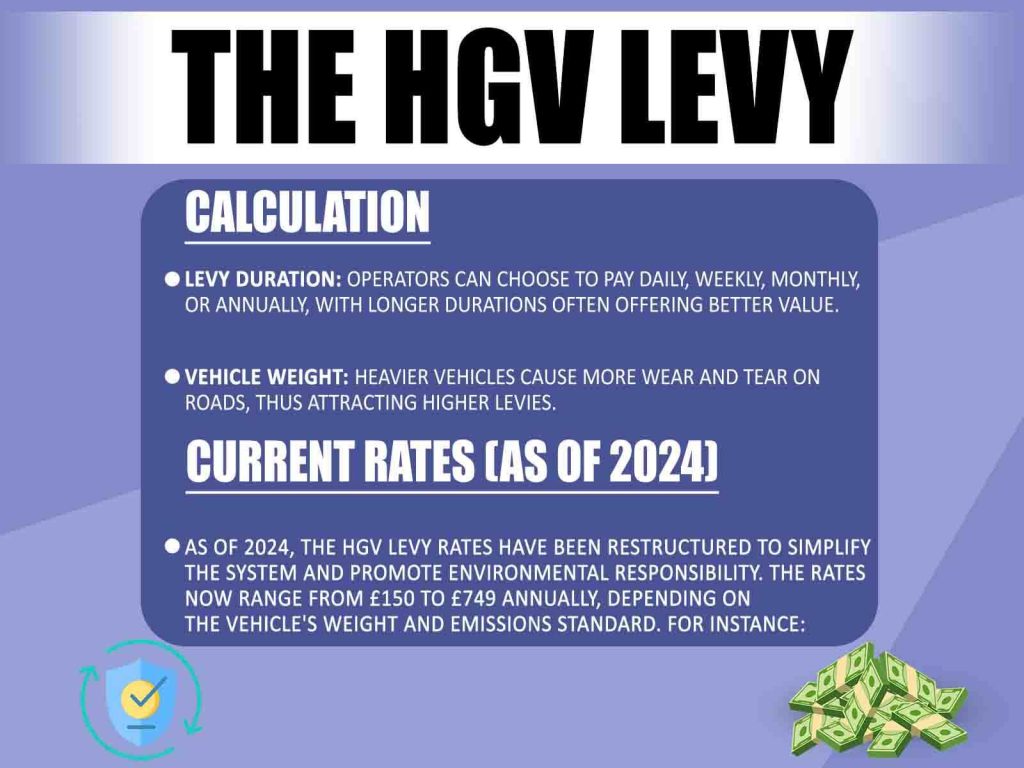

Calculation

The levy amount is determined based on several factors:

- Vehicle Weight: Heavier vehicles cause more wear and tear on roads, thus attracting higher levies.

- Emissions Standard: Vehicles meeting higher Euro emissions standards (e.g., Euro VI) benefit from lower rates.

- Levy Duration: Operators can choose to pay daily, weekly, monthly, or annually, with longer durations often offering better value.

This tiered structure incentivizes the use of cleaner, more efficient vehicles and allows flexibility in payment options.

Current Rates (as of 2024)

As of 2024, the HGV levy rates have been restructured to simplify the system and promote environmental responsibility. The rates now range from £150 to £749 annually, depending on the vehicle’s weight and emissions standard. For instance:

- Euro VI vehicles (12–31 tonnes): £150 per year

- Older vehicles (same weight): £195 per year

- Euro VI vehicles (over 38 tonnes): Up to £749 per year

This adjustment aims to encourage the adoption of cleaner vehicles by offering financial incentives to operators who invest in environmentally friendly technology.

Payment

For UK-registered vehicles, the HGV levy is incorporated into the Vehicle Excise Duty (VED) and is paid alongside it, either annually or semi-annually. Foreign-registered vehicles must pay the levy before entering the UK, which can be done through the online HGV levy service.

Payment options include daily, weekly, monthly, or annual rates, providing flexibility for international operators.

Compliance

Ensuring compliance with the HGV levy is crucial. The Driver and Vehicle Standards Agency (DVSA) employs Automatic Number Plate Recognition (ANPR) technology and conducts roadside checks to identify non-compliant vehicles.

Failure to pay the levy can result in significant fines and penalties, emphasizing the importance of timely and accurate payments.

Checking Levy Status

Operators can verify the levy status of their vehicles using the online HGV levy service. By entering the vehicle’s registration details, users can confirm payment status, view due dates, and manage their accounts. This tool is essential for maintaining compliance and avoiding potential penalties.

Recent Changes

In August 2023, the UK government revised the HGV levy structure to reduce the number of rate categories from 22 to 6, simplifying the system for operators.

Additionally, the highest annual levy rate was reduced from just under £1,000 to £749, easing the financial burden on hauliers.

These changes reflect the government’s commitment to supporting the transport industry while promoting environmental sustainability.

Future of the Levy (2025)

Looking ahead to 2025, the HGV levy is set to increase in line with the Retail Price Index (RPI), reflecting inflationary trends.

This adjustment ensures that the levy continues to contribute effectively to road maintenance funding. Operators should anticipate these changes and plan accordingly to accommodate the updated rates.

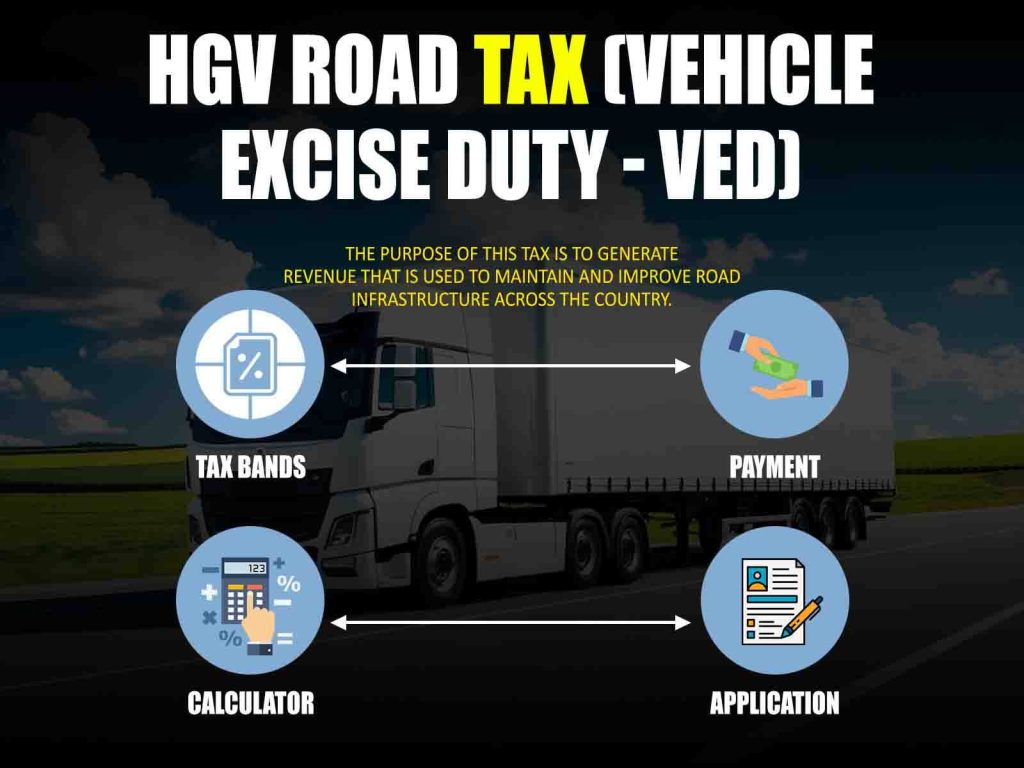

HGV Road Tax (Vehicle Excise Duty – VED)

Purpose

HGV road tax, also known as Vehicle Excise Duty (VED), is a tax that applies to all vehicles used on UK roads, including HGVs. The purpose of this tax is to generate revenue that is used to maintain and improve road infrastructure across the country.

Unlike the HGV levy, which is specifically aimed at heavy goods vehicles, VED applies to all vehicles, including private cars, motorcycles, and commercial vehicles.

For HGVs, the road tax amount is influenced by several factors, including the weight of the vehicle and its emissions standard. This helps ensure that vehicles causing more wear and tear on the road network contribute a fairer share to the maintenance costs.

Calculation

VED for HGVs is calculated based on a vehicle’s gross weight and emissions standard. The more weight a vehicle carries and the higher its emissions, the higher the tax will be. For example:

- Euro VI-compliant vehicles (the most environmentally friendly standard) will generally face lower VED rates compared to older vehicles with higher emissions.

- Heavy vehicles that exceed certain weight thresholds (e.g., vehicles over 12 tonnes) are subject to higher rates.

Additionally, the calculation takes into account whether the vehicle is used for private or commercial purposes, with commercial vehicles generally paying higher rates.

Tax Bands

VED for HGVs is grouped into tax bands based on vehicle weight and emissions:

- Under 12 tonnes: These vehicles typically fall into the lowest tax bands, ranging from £200 to £500 annually.

- 12 to 32 tonnes: These vehicles will face higher rates, generally between £500 and £1,000 annually.

- Over 32 tonnes: The largest HGVs will be taxed at the highest rates, which can exceed £1,500 annually.

The specific rate for each vehicle depends on its weight and emissions, with more polluting vehicles attracting higher fees.

Payment

Like the HGV levy, HGV road tax is typically paid annually, although operators can also pay semi-annually or quarterly. The payment can be made directly through the DVLA’s website, via post, or through an authorized agent.

For international hauliers operating in the UK, road tax can be paid for short durations, such as a month or a week, allowing flexibility for operators who may not be in the country for long periods.

Application

To apply for HGV road tax, operators need to provide the vehicle’s registration number, proof of insurance, and MOT test certificate. The MOT certificate ensures that the vehicle meets the required safety standards and emissions regulations, which is a key part of the road tax application process.

In cases where the vehicle has not been previously taxed, operators must also provide proof of vehicle identification and registration details, which can be obtained from the DVLA.

Calculator

To help operators estimate the road tax due on their HGVs, the DVLA provides an online road tax calculator. This tool enables users to input the vehicle’s details (e.g., weight and emissions standard) to calculate the exact amount of road tax owed. This is an essential resource for ensuring accurate payments and avoiding penalties for underpayment.

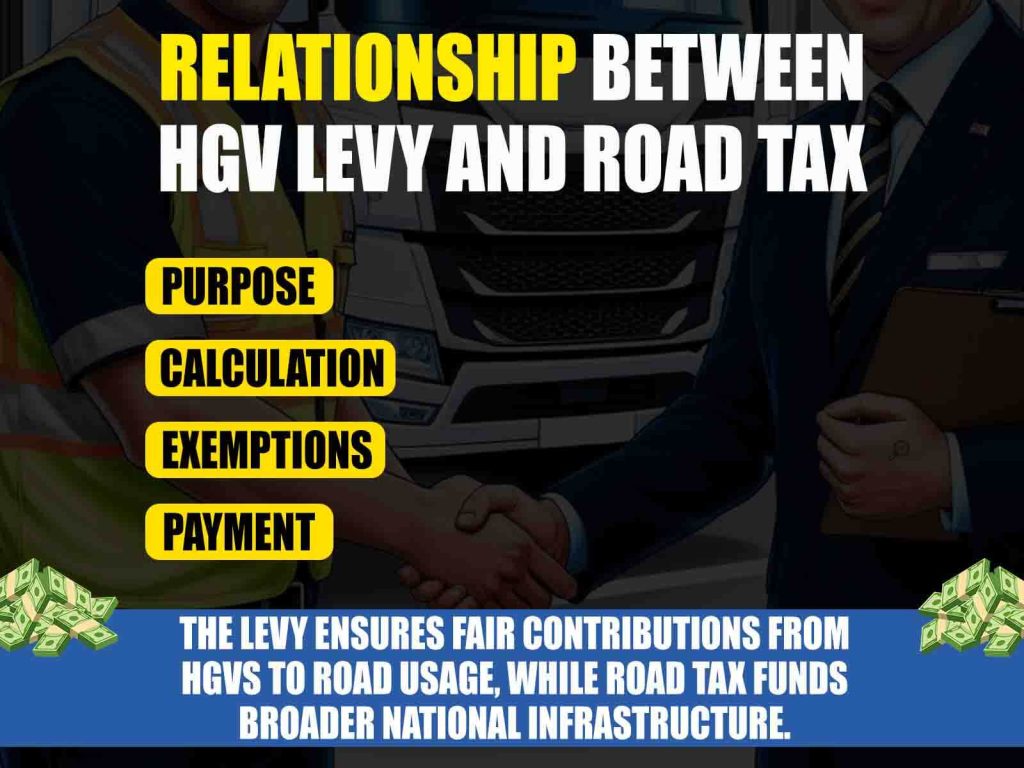

Relationship Between HGV Levy and Road Tax

While both the HGV levy and road tax apply to heavy goods vehicles (HGVs), they serve different purposes and are calculated differently. Understanding their relationship is crucial for compliance.

Key Differences Between HGV Levy and Road Tax

Purpose:

The HGV levy targets road usage by HGVs, helping fund road maintenance and infrastructure. It applies to vehicles over 12,000 kg, regardless of emissions or road tax status. In contrast, road tax (VED) funds national road maintenance for all vehicles.

Calculation:

The HGV levy is based on vehicle weight and emissions standards, with flexible payment options (daily to annual). Road tax is calculated based on gross weight and emissions class (e.g., Euro VI), with fewer payment options.

Exemptions:

Some vehicles, like those used for agriculture or historic purposes, may be exempt from the HGV levy. Road tax exemptions are typically for non-commercial vehicles or those meeting specific criteria (e.g., electric vehicles).

Payment:

The HGV levy is paid through the DVLA or an online service, either before entering the UK or annually for domestic vehicles. Road tax is paid via the DVLA, with options for annual, semi-annual, or quarterly payments.

Complementary Roles

Although they serve different purposes, both the HGV levy and road tax work together. The levy ensures fair contributions from HGVs to road usage, while road tax funds broader national infrastructure. Operators must comply with both taxes to avoid fines, as some international hauliers may pay both in a single transaction when entering the UK.g the UK.

Key Considerations for HGV Operators

HGV operators must consider several factors to ensure compliance with both the HGV levy and HGV road tax. These include budgeting, emissions standards, international compliance, record-keeping, and planning for future changes.

1. Budgeting for Tax and Levy Costs

It’s essential for operators to budget for both HGV levy and road tax. Costs depend on vehicle weight, emissions, and payment duration. Short-term options may suit seasonal operators, while an annual payment might benefit those with a stable fleet.

2. Emissions Standards and Vehicle Upgrades

Vehicles with higher emissions incur higher taxes. Upgrading to newer, Euro VI vehicles can lower both the HGV levy and road tax. Operators should assess their fleet and plan for efficient upgrades to reduce costs and meet environmental standards.

3. International Hauliers and Cross-Border Compliance

International hauliers need to ensure compliance with both the HGV levy and road tax when entering the UK. HGV levy payments should be made before entry, while road tax may require short-term payments for foreign vehicles. Non-compliance can lead to fines and delays.

4. Record Keeping and Compliance

Operators should keep accurate records of tax payments for both the HGV levy and road tax. This helps avoid penalties during audits or inspections. Fleet management software can streamline the process, ensuring compliance and timely renewals.

5. Planning for Future Increases

The HGV levy will increase in 2025 in line with the Retail Price Index (RPI). Operators should prepare for these hikes and stay updated on any changes to road tax or transport regulations to avoid unexpected costs.

Conclusion

Understanding the HGV levy and road tax is essential for operators to ensure compliance and effective vehicle management. While both taxes apply to heavy goods vehicles, they serve distinct purposes and are calculated differently. The HGV levy focuses on contributions to road infrastructure based on the vehicle’s weight and emissions, while road tax supports national road maintenance across all vehicle types.

By maintaining proper records, planning for future cost increases, and staying up-to-date with the regulations, operators can manage both taxes effectively. Non-compliance with either tax can result in fines, penalties, and delays, making it crucial for operators to stay informed and proactive.

FAQs

The HGV levy is a charge on heavy goods vehicles to contribute to road infrastructure maintenance.

HGV road tax is based on the vehicle’s weight and emissions class.

Yes, vehicles like agricultural or historic ones may be exempt from the HGV levy.

Yes, international hauliers can pay both taxes in a single transaction when entering the UK.

Yes, the HGV levy rates will increase in 2025, aligned with the Retail Price Index (RPI).

Yes, you can check the status of your levy via the DVLA or online services.

Source / Ref.: Gov.uk Contains public sector information licensed under Open Government Licence v3.0.

Written by [Ketan Borada / British Portal Team] – Founder of British Portal, dedicated to providing accurate and up-to-date information on UK public services and benefits.Related Posts

Previous Post

Next Post

Previous Post

Next Post

- Business

5

5 - Cricket5

- Department for Education49

- Departments3

- Driving and Transport

53

53 - Education45

- Finance6

- Football13

- Golf3

- Government

108

108 - Guides1

- Health4

- Health

5

5 - International Politics9

- Law and Justice31

- Money and Tax23

- National Politics4

- News68

- Politics6

- Sports38

- Technology5

- Tennis3

- Transportation4

- Uncategorized4

- Visa

17

17 - Visas and Immigration

24

24 - Weather1