UK Education Loans for International Students – Complete Guide

International students believe education to be a dream. However with increasing tuition and living costs money is many times needed. Luckily, today, education loans have been made available, for helping students in financing the study costs. In this guide, information on UK education loans for international students, will be provided in simple and easy terms .

Why Education Loans are Needed by International Students?

First and foremost, studying in the UK is costly. Tuition, Accommodation, Meals, Transport – all everything costs are a high burden. So, loans for students have been opted for by the thousands of students each year. Also, since the UK universities have a high reputation, loans for students studying in college are being thought of as wise investments. IN general, a return on education is realized as a high-paying career upon graduation.

Who Can Apply for Student Loan in the UK?

Not everyone is eligible. But, loans are being granted when this condition is met:

1.Application should be made to a UK based university.

2.A co-applicant (usually parent/guardian) is usually needed.

3.Academic performance must be satisfactory.

4.A proper visa must be issued.

Where to Apply for UK Education Loans?

Here is a list of trusted UK based banks and private lenders for students who will be applying for education loans or financial support if planning to study in UK:

UK Banks

1.HSBC UK

Use easy finance management to apply for a student account with interest free overdrafts.

2.Barclays Bank

Offers a Student Additions Account with flexible banking and student perks.

3.Lloyds Bank

Offers tiered overdraft facilities to student accounts and also controls them online.

4.NatWest Bank

Called well known for student benefits such as rail cards and budgeting tools.

5.Santander UK

Offers the 123 Student Account with a free 4-year rail card and up to £2,000 overdraft.

6.Royal Bank of Scotland (RBS)

Perfect when used with budgeting apps and overdraft options for managing student expenses.

Private Student Loan Providers in the UK

1.Future Finance

Provides student loans to UK and international students.

2.Lendwise

May be useful for postgraduate students seeking tuition costs or living costs support.

3.Prodigy Finance

Loan offers to international students (no collateral necessary).

4.MPower Financing

Offers funding to international students studying in the UK’s universities.

How to Increase Your Chances of Loan Approval?

Students should seek admission with a trustworthy co-applicant who maintains stable earnings.

1.Choose a reputed university/course

2. Maintain a good academic record

3.Show clear repayment capacity

4.Offer collateral (for higher loan amounts)

5.Include valid visa proof and financial plan

What is the Loan Limit?

It depends on the lender:

1.With collateral: Up to ₹1.5 Cr

2.Without collateral: Up to ₹45–50 Lakhs

3.Covers tuition, living, travel, and insurance expenses

How Long Does It Take to Get Disbursed?

The disbursement or getting of the education loans or student finance in UK is later on depending upon the type of funding or lender you have chosen.

UK Government Student Finance (via Student Finance England)

1.Disbursement Time:

Generally 3–5 working days after the beginning of your course and your university confirms that you are enrolled.

2.Tuition fee loan Payment:

This is paid directly to your university, maintenance loan will go into your bank account and paid 3 times in the terms.

UK Banks (with student accounts)

1.Student account overdraft:

In case your parents open a student account (providing HSBC, Barclays, Lloyds, etc) you can usually get access to your interest free overdraft right away or in a few days from the moment your account has been approved and verified.

Private Loan Providers (like Prodigy Finance, Future Finance)

1.Forecast disbursement time:

Generally 7 to 14 working days after the final approved and signing agreement.

Please note that some lenders will send the funds directly to the university, whereas some will send to your UK bank account.

How to Repay the Loan?

UK Government Student Loan (via Student Finance England)

1.Repayment Starts:

Not until you graduate with income above that repayment threshold (currently £27,295 a year for Plan 2 loans).

2.How Much You Repay:

What you pay is 9% of your income over the threshold.

3.Automatic Deduction:

There is no work involved as payments are automatically deducted from your salary through PAYE (Pay As You Earn).

4.Loan Write-off:

The remaining sum is written off if the loan is not fully repaid within 30 years.

Private Loan Providers

1.Repayment Starts:

The grace period after graduation may be different for some lenders and some do not allow a grace period of 6 months after graduation.

2.Monthly Instalments:

EMI plans fixed or flexible depending upon your loan agreement. These are normally paid back by bank or direct debits.

3.Interest Rate:

Depending on your credit profile, co-signer or course. So plan your budget accordingly because normally higher than government loans.

4.International Repayment:

Once you complete your studies you do repay by international transfer or local bank arrangements if you return to India or go to any other country.

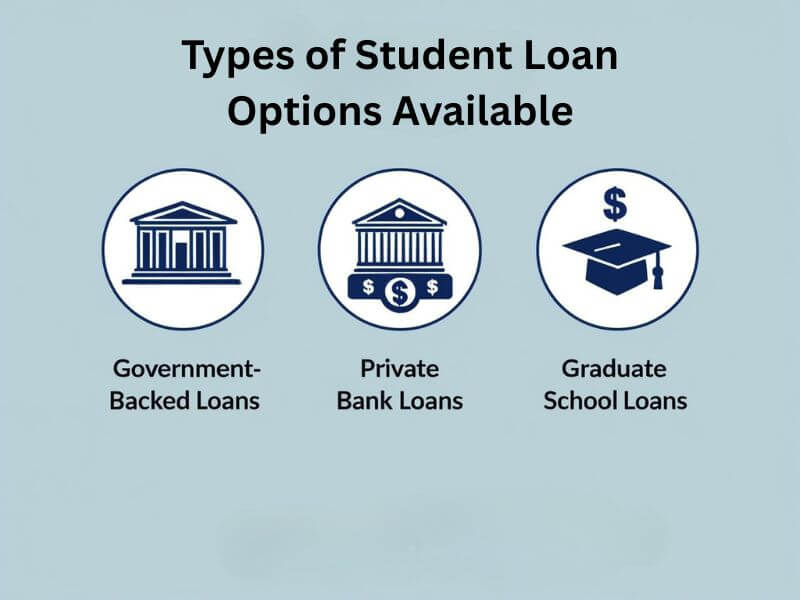

Types of Student Loan Options Available

1.Government-Backed Loans

Despite most student loan options from the UK government being open to home students, some scholarships and funding assistance for international students are also available from time to time.

2. Private Bank Loans

Many a time, personal student loan is opted over because of quick application process and flexible procedure of repayment. These loans are generally provided based on the quality of the university ranking, course type as well as how much the students are expected to expect in terms of their future income.

3.Graduate School Loans

For individuals acquiring a Master’s or PhD in the UK, graduate school loans are being offered upfront by overseas lending agencies, or home country banks.

Steps to Apply for Student Loan in the UK

This is how the application for loan student process basically is conducted

1.First a place at a UK university must be gained.

2.After that, all important documents such as passport, admission letter, fee structure, etc. are gathered.

3.After this the loan application must be fulfilled and submitted.

4.Finally after breaching of documents loan is approved.

Moreover, top college student loans are frequently given to students with excellent grades scores and admission positions in UK universities.

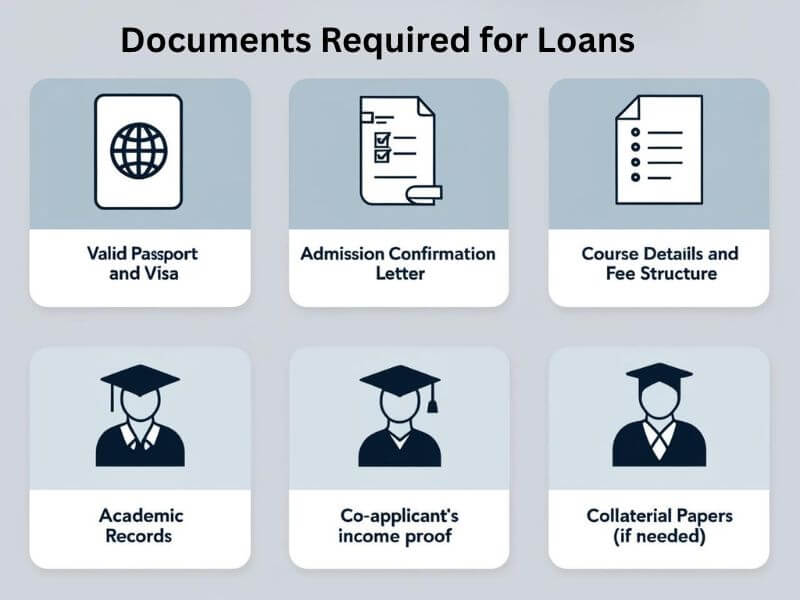

What Documents Are Required?

Before any loan approval, these documents are most likely asked for

1.Valid Passport and Visa

2.Admission Confirmation Letter

3.Course Details and Fee Structure

4.Academic Records

5.Co-Applicant’s Income Proof

6.Collateral Papers (if needed)

Tips for Choosing the Best Student Loans for College

Not many student loan options are available, but the one you have to choose must be selected carefully. So, below are some helpful pointers

1.Always compare interest rates

2.Find out if there is a borrowers deferment

3.Know all terms and condition prior to signing

4.Go for student loans for college that are with minimal processing fees and repayment possibilities flexible

Repayment and Conditions

After completing studies, repayment begins. Typically, personal student loans have a payoff timeline of 5-10 years depending on the lender. Generally, a moratorium is being provided, where in there will not be any EMI in most cases. However, interest is may still be charged. Thus, smart strategy is required for intelligent education loans management.

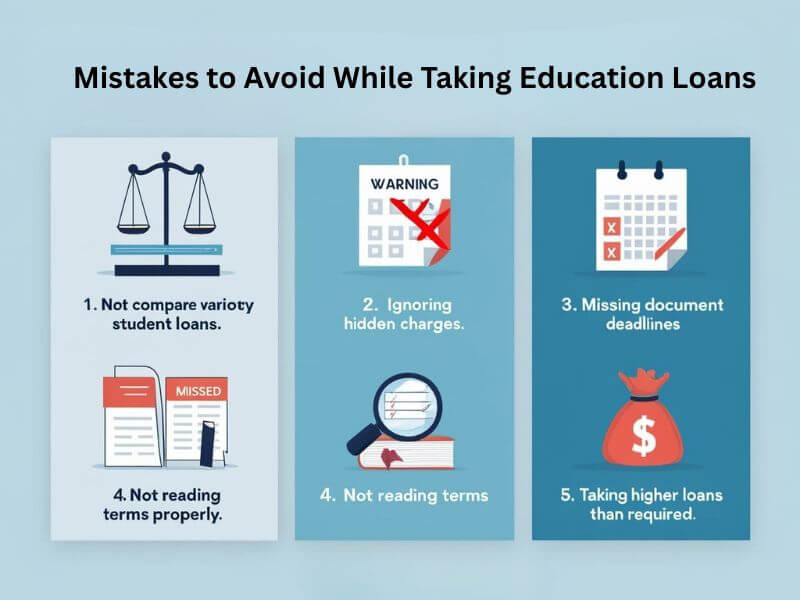

Mistakes to Avoid While Taking Education Loans

Often, the students are a victim of such as these mistakes:

1.Not comparing various student loans

2.Ignoring hidden charges

3.Missing document deadlines

4.Not reading terms properly

5.Taking higher loans than required

Conclusion

Today, going to study in UK is not in closed, even for middle-class family is not a problem. Through well-planned education loans, increasing number of foreign students are fulfilling their academic dreams. From student loans for college students, graduate school loans to personal student loans, your future is secure. However, always remember loans shall be beneficial to you if used correctly.

FAQ

Yes, education loans are being given to international students by banks at home country and international lenders. These loans are to pay for tuition fees, living costs and travel expenses while studying in the UK.

Applying for loan, admission approval is needed first. Then, the important documents which include the offer letter, passport, fee structure and the income proof of co-applicant are submitted to the bank. All that needs to be done is verification and the sanction and disbursal of the loan.

Top student loans for college will offer the lowest interest rates, no surprise charges, and flexible repayment considering the fact that. Some of the other popular options are loans from SBI Global Ed-Vantage , Prodigy Finance, among others.

Repayment always starts after the course and this is around 6 to 12 months. Most of the post graduate loan and personal student loan provides amnesty period in which the EMI is not required. However, please check the exact details with your lender.

Read More Posts

Written by [Ketan Borada / British Portal Team] – Founder of British Portal, dedicated to providing accurate and up-to-date information on UK public services and benefits.

Related Posts

Previous Post

Next Post

- Business

5

5 - Cricket5

- Department for Education49

- Departments3

- Driving and Transport

53

53 - Education45

- Finance6

- Football13

- Golf3

- Government

108

108 - Guides1

- Health

5

5 - Health4

- International Politics9

- Law and Justice31

- Money and Tax23

- National Politics4

- News68

- Politics6

- Sports38

- Technology5

- Tennis3

- Transportation4

- Uncategorized4

- Visa

17

17 - Visas and Immigration

24

24 - Weather1